This annual report will be presented to Parliament to meet the statutory reporting requirements of the Compulsory Third Party Insurance Regulation Act 2016.

This report is verified to be accurate for the purposes of annual reporting to the Parliament of South Australia.

David Price

Chief Executive & CTP Regulator

From the Chief Executive

First, I would like to thank Kim Birch, the outgoing Regulator, for her stewardship of the privately underwritten Scheme since it began in 2016.

Kim oversaw and shaped a competitive and efficient scheme with a person-centred approach that has delivered for the South Australian community. Kim’s dedication to the role has left a marked impact and set the Scheme and the Regulator’s office in good stead for the future.

This past year we have maintained our focus on simplification, reducing regulatory burden and delivering improvements aimed at benefiting injured people and motorists.

The CTP Scheme has continued to deliver a fair and competitive scheme with choice, ease and confidence for the South Australian community with CTP premiums reducing as of 1 July 2024 for 99% of registered motor vehicles.

The Regulator team continues to work with key scheme stakeholders, including major SA hospital trauma units, to increase awareness and knowledge of the Scheme to encourage early intervention and connect injured people with CTP Insurers.

Over the coming year, we will continue our work to deepen engagement with scheme stakeholders and strengthen the communication materials available for the community to better understand the Scheme.

The team undertook a holistic review of the Regulator Rules and Commercial Rules (Scheme Rules) with an emphasis on simplification for injured people and updating insurer requirements to reflect the current focus of the Scheme.

After an extensive review process, new Scheme Rules were implemented on 1 July 2024.

These rules set out the obligations of CTP Insurers and can be referred to by injured people to understand how the Scheme operates. We also implemented a new compliance management system for recording and monitoring insurer compliance with scheme requirements.

This new system strengthens the Regulator’s compliance monitoring capabilities for CTP Insurers, improves the efficiency of audit processes and will continue to support the Regulator’s oversight of insurers into the future.

Technological advancements have the potential to transform many aspects of the Scheme, including regulatory monitoring and service delivery. While this presents opportunities for improvements to scheme efficiency and the experience of injured people and motorists, it also poses challenges for the Scheme to ensure changes benefit our community.

I look forward to continuing my work at the Regulator by leading the team in its engagement with scheme stakeholders to support the community in the coming years.

David Price, Chief Executive and CTP Regulator

Overview

The Compulsory Third Party (CTP) Insurance Scheme is governed by South Australian

legislation in the following Acts of State Parliament: Motor Vehicles Act 1959 (MV Act), Civil

Liability Act 1936 (CL Act) and Compulsory Third Party Insurance Regulation Act 2016 in addition to contracts between the State and government approved insurers (CTP Insurers).

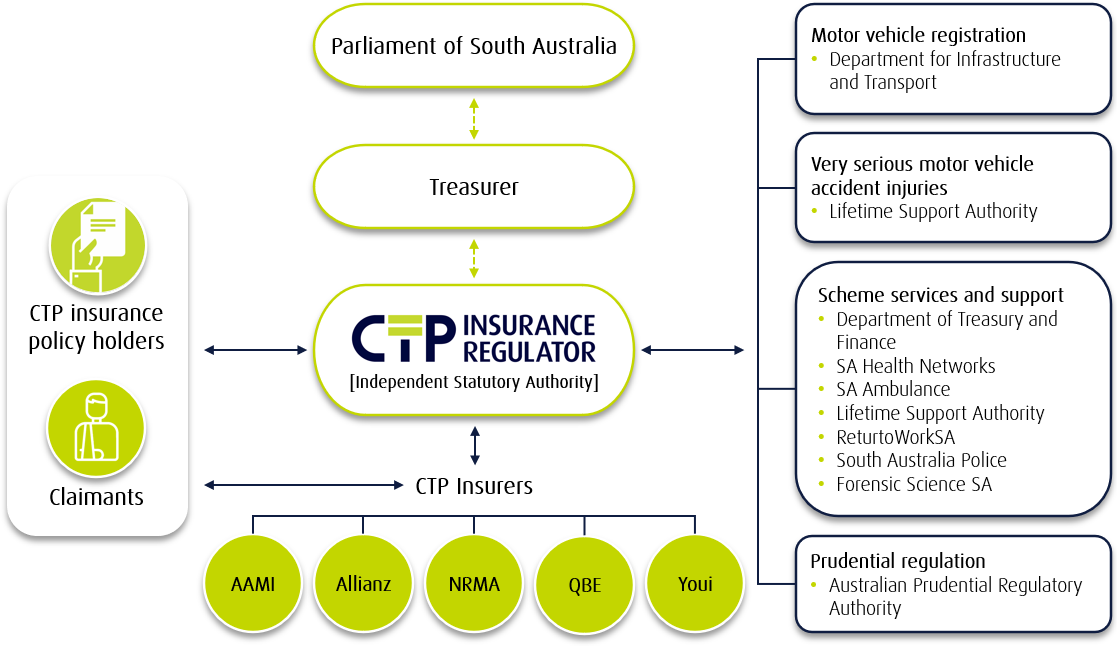

The CTP Regulator oversees the Scheme and regulates the CTP Insurers, AAMI, Allianz, QBE,

NRMA and Youi. Fundamental aspects of the Scheme are to support the recovery of people

injured in motor vehicle accidents and provide a compulsory Policy of Insurance (policy) to

protect motor vehicle owners against the financial impact of causing personal injury or death to other road users through the use of their vehicle anywhere in Australia.

CTP insurance is paid for at the same time as motor vehicle registration. The policy attaches

to the vehicle, not the purchaser. The minimum terms and conditions of the policy, set by the Regulator, are available on the Regulator’s website www.ctp.sa.gov.au. (external site) (external site)

Motorists actively choose their CTP Insurer based on factors including price, brand, claimant service rating and approved incentives. The CTP Insurers underwrite the South Australian Scheme and manage claims against the policy.

In South Australia, claims for compensation under the Scheme are fault-based common law claims modified by statute, primarily the CL Act. This means injured road users may be eligible for injury recovery support, payment of reasonable and necessary treatment and

compensation when another party is at fault or partially at fault. Access to compensation

requires the injured person’s injuries to meet thresholds depending on their seriousness.

The Regulator is appointed as the Nominal Defendant under Part 4 of the MV Act. Nominal

Defendant claims arise when the vehicle responsible for a motor vehicle accident in South

Australia that results in injuries or death to other road users is either uninsured or unidentified. The Regulator assigns management of Nominal Defendant claims to the CTP Insurers in line with their market shares.

The Scheme also provides funding for reasonable and necessary treatment, care and support for children injured while under the age of 16 years in an accident in South Australia, regardless of fault.

The CTP Scheme is complemented by the Lifetime Support Scheme which operates separate from the CTP Scheme. The Lifetime Support Scheme is a no-fault scheme which provides treatment, care and support for people who have sustained very serious injuries in motor vehicle accidents in South Australia.

The Regulator is established as an independent statutory authority under the Compulsory Third Party Insurance Regulation Act 2016 (the Act). The Regulator’s functions are set out in section 5(1) of the Act.

The Regulator is responsible for:

- regulating CTP Insurers

- monitoring and reviewing the operations and efficiency of the CTP Scheme

- oversight, monitoring and reporting of CTP Insurer activities

- determining the minimum terms and conditions of the policy of insurance

- determining CTP premiums

- providing information to consumers about the Scheme and CTP Insurers.

The CTP Regulator's vision is to deliver a fair and competitive CTP Scheme with choice, ease

and confidence for the South Australian community.

To provide community confidence in the Scheme by regulating CTP Insurers and monitoring the performance of the CTP Scheme.

| Our values | What this means for us |

|---|---|

| Outcomes driven |

|

| Accountable |

|

| Collaborative |

|

| Fair |

|

| Supportive |

|

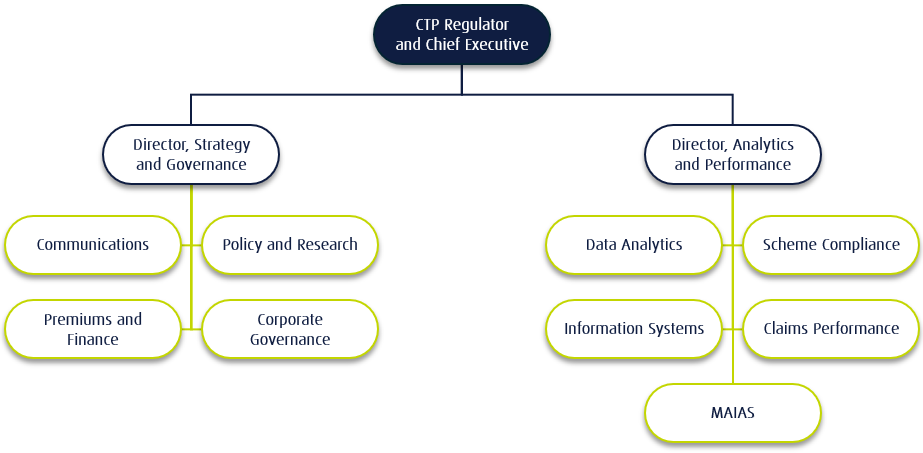

Changes to the CTP Regulator

During 2023-24 the following changes were made to the Regulator's structure

- MAIAS was transferred to the portfolio of Director, Analytics and Performance

As of 6 July 2024, David Price is the Chief Executive (CE) and CTP Regulator (Regulator),

responsible for carrying out the functions of the Regulator and the CE as determined by the

Compulsory Third Party Insurance Regulation Act 2016. The Regulator is also the Motor

Accident Injury Accreditation Scheme (MAIAS) Administrator. Prior to 6 July, Kim Birch was the Regulator and CE.

Until 6 July David Price was the Director, Strategy and Governance, responsible for scheme research and policy, providing information to motorists, overseeing corporate functions including finance and the process of determining premium ranges for premium classes.

Ivan Lebedev is the Director, Analytics and Performance, responsible for information systems, data analytics, monitoring the Scheme, CTP Insurer performance and the MAIAS.

- Compulsory Third Party Insurance Regulation Act 2016

- Part 4, Motor Vehicles Act 1959

The Regulator has a service level agreement with the Department of Treasury and Finance

(DTF) for the provision of corporate services to keep administration costs down and support the effective functioning of the Regulator’s office.

Our significant relationships to support scheme efficiency and administration are with the:

- Department for Infrastructure and Transport for the collection and disbursement of CTP premiums

- Lifetime Support Authority and ReturntoWorkSA to improve recovery outcomes for injured people

- Australian Prudential Regulation Authority to monitor the financial stability and solvency of the CTP Insurers.

government agencies to provide the following services to the Scheme:

- Road safety: Department for Infrastructure and Transport and South Australia Police

- Health and Emergency Services: Department for Health and Wellbeing; SA Ambulance Service; State Rescue Helicopter Service; Forensic Science SA

- Customer support and transaction processing: Department for Infrastructure and Transport.

MoAAs are funded from the administrative component of CTP premiums, collectively known as the CTP Scheme Services fee. The CTP Scheme Services fees are detailed on page 27.

CTP Regulator stakeholders:

The Regulator is appointed as the Motor Accident Injury Accreditation Scheme (MAIAS)

Administrator by the designated Minister under section 76 of the Civil Liability Act 1936. The

MAIAS Administrator has administrative and financial responsibility of the MAIAS which was

established to accredit health professionals to undertake Injury Scale Value (ISV) medical

assessments.

An ISV medical assessment is used to assist in determining an injured road user’s entitlement to compensation by assigning referred injuries to ISV item numbers listed in Schedule 1 of the Civil Liability Regulations 2013. The ISV is a number between 0 and 100 that reflects the level of adverse impact of the injury on the person, based on medical evidence.

The MAIAS Administrator uses the MAIAS Rules to oversee the performance of the accredited medical practitioners. The Rules prescribe the regulatory and service standards required for medical practitioners to achieve and maintain accreditation.

The key objective of MAIAS is to create an independent system that provides consistent,

objective and reliable ISV medical assessments. As administrator of MAIAS, the Regulator’s

responsibilities include but are not limited to:

- prescribing the processes and documentation of the MAIAS including accreditation training courses and overseeing their implementation

- supporting Accredited Medical Practitioners (AMPs) and monitoring their performance to verify conformity with accreditation obligations

- making recommendations to the Minister for approval of applicants who meet the accreditation criteria

- maintaining and keeping an up-to-date register of all AMPs

- continuing oversight of the MAIAS.

The Regulator's performance

In 2023-24, the Regulator continued to deliver on its strategic objectives to support the CTP

Scheme. Highlights include:

- Redetermined CTP premium bands which saw a decrease in the lowest available premiums for 99.9% of motorists from 1 July 2024.

- Conducted insurer audits to monitor compliance of CTP Insurers with contractual and legislative obligations of the Scheme. See page 19 for more detail.

- Continued our program of surveys with injured people to gain insight into insurer claimant service. The results of these surveys are published as the claimant service rating for each insurer on registration renewal notices and the CTP website to assist vehicle owners to choose an insurer.

- Reviewing, developing and publishing an updated set of Scheme Rules to provide better regulation and reduce unnecessary regulatory burden. See page 18 for more detail.

- Implemented a new compliance management system for recording and monitoring insurer compliance with scheme requirements. See page 21 for more detail.

- Conducted a thorough refurbishment of CTP website content to ensure that content is accessible and easy to understand to support the South Australian public’s understanding of the CTP Scheme. See page 19 for more detail.

The Regulator’s strategic objectives support delivery of statutory functions under section 5 of the Compulsory Third Party Insurance Regulation Act 2016.

The Regulator’s performance against strategic objectives is summarised below.

| Performance indicator | Target date | Outcome |

|---|---|---|

| Objective 1: Oversee a financially sustainable, effective and efficient scheme | ||

| Undertake mid-year review of premium bands | November 2023 | ✓Achieved |

|

Annual premium bands reviewed and set for each premium class to apply from 1 July 2024 | May 2024 | ✓Achieved |

|

Plan and prepare the Scheme for emerging technologies and participate in Across Government Automated Vehicle Reform Working Groups | December 2027 | On track |

|

Conduct MAIAS Quality Assurance program (see page 24) | June 2024 | ✓Achieved |

| Performance indicator | Target date | Outcome |

|---|---|---|

| Objective 2: Promote an outcome driven, early recovery and service focused approach to claims management | ||

|

Research, identify and implement injury recovery and scheme experience initiatives that improve outcomes and experience of injured people in the Scheme | June 2024 | ✓Achieved |

|

Deepen engagement with hospitals and rehabilitation centres to promote early intervention and transition to the Scheme | February 2024 | ✓Achieved |

|

Identify opportunities to standardise insurer compliance requirements across jurisdictions (see page 18) | June 2024 | ✓Achieved |

|

Explore the expansion of MAIAS peer reviewers (see page 25) | September 2023 | ✓Achieved |

|

Analyse when and why Independent Medical Assessments are used for actionable insights to support a positive experience for injured people (see page 22) | June 2024 | ✓Achieved |

|

Review how working injured people with CTP claims return to work to monitor and encourage insurer supports | December 2024 | On track |

|

Conduct a review of Scheme Rules and contracts between the State and CTP Insurers (see page 18) | June 2024 | ✓Achieved |

|

Review insurer benchmark for assessing insurer liability timing (see page 23) | April 2024 | ✓Achieved |

|

Develop an IT solution to support Regulator compliance activities (see page 21) | December 2023 | ✓Achieved |

| Objective 3: Deliver a customer centric focus | ||

|---|---|---|

|

Digitalise CTP Regulator processes to standardise and improve consistency | June 2024 | ✓Achieved |

| Performance indicator | Target date | Outcome |

|

Identify and implement improvements to enhance online injury claim form | June 2024 | ✓Achieved |

|

Review and refresh Regulator website (see page 19) | June 2024 | ✓Achieved |

|

Implement customer centric innovations explored as enablers for injured people to manage their own claim (see page 19) | June 2024 | ✓Achieved |

| Objective 4: Enhance the capability of the team | ||

|

Implement strategies to strengthen our resilient and contemporary team | June 2026 | On track |

|

Implement and embed project management tool enhancements and updated Framework | June 2024 | ✓Achieved |

|

Provide opportunities to develop staff capability through cross-skilling across teams | June 2026 | On track |

Capacity Building Placement

The Regulator runs a Capacity Building Placement for people with disability. The program

creates the opportunity for people with disability to gain employment skills and confidence,

in a supportive environment. The program also works towards building a diverse and inclusive public sector where everyone belongs.

The program aims to support strengthening the capability and confidence of the participant to compete in the jobs market and provides a blueprint to share with others to establish similar programs in their organisations.

The most recent participant finished their placement having achieved employment in the

private sector. The program will continue in the next financial year with a new participant

joining the Regulator team.

Regulator staff access the Department of Treasury and Finance’s (DTF) performance

discussion and development systems, including the new organisational development tool,

myCareer. Training has been undertaken to ensure the Regulator is using the system to its

full capacity and supports the Regulator’s learning and development strategies.

All staff have individual performance plans in place that are discussed at least every six

months.

Regulator staff are employed by DTF and seconded to the Regulator. Regulator staff access

DTF’s work health, safety and return to work programs.

Regulator staff work health and safety breaches, workplace injury claims, notifiable incidents or improvement and prohibition notices are recorded and reported in the DTF annual report.

Regulator management staff undertook a wellbeing training course, Be Well Masterclass –

People Leader, offered by DTF to support the wellbeing of employees. Wellbeing training will continue in the next financial year, providing the opportunity for all Regulator employees to undertake wellbeing training.

SA Government People Matter Employee Survey

Regulator staff participated in the SA Government People Matter Employee Survey. Survey

results will be available to the Regulator by the end of 2024. The views of our staff will inform the actions of the Regulator and the public sector more generally in the coming years. In particular, we will look for opportunities to enhance workplace culture, policies and practices that support our team and make the public sector a better place to work for everyone.

| Executive classification | Number of executives |

|---|---|

| SAES Level 1 | 2 |

| SAES Level 2 | 1 |

The Office of the Commissioner for Public Sector Employment (external site) (external site) has a workforce information (external site) (external site)

page that provides further information on the breakdown of executive gender, salary and

tenure by agency.

Financial performance

The following is a summary of the overall financial position of the CTP Regulator. This

information is unaudited. Full audited financial statements for 2023-2024 are attached to this report.

| Statement of Comprehensive Income | 2023-24 Budget $000s | 2023-24 | Variation $000s | 2022-23 Actual $000s |

|---|---|---|---|---|

| Total Income | 68,610 | 74,443 | 5,833 | 68,947 |

| Total Expenses | 68,941 | 67,369 | (1,572) | 64,750 |

| Net Result | (331) | 7,074 | 7,405 | 4,197 |

| Total Comprehensive Result | (331) | 7,074 | 7,405 | 4,197 |

| Statement of Financial Position | 2023-24 Budget $000s | 2023-24 Actual $000s | Variation $000s | 2022-23 Actual $000s |

|---|---|---|---|---|

| Current assets | 53,232 | 55,391 | 2,159 | 48,505 |

| Non-current assets | 174 | 235 | 61 | 174 |

| Total assets | 53,406 | 55,626 | 2,220 | 48,679 |

| Current liabilities | 15,247 | 10,244 | (5,003) | 10,431 |

| Non-current liabilities | 466 | 526 | 60 | 466 |

| Total liabilities | 15,713 | 10,770 | (4,943) | 10,897 |

| Net assets | 37,693 | 44,856 | 7,163 | 37,782 |

| Equity | 37,693 | 44,856 | 7,163 | 37,782 |

The following is a summary of external consultants that have been engaged by the CTP

Regulator, the nature of work undertaken and the actual payments expensed for the work

undertaken during the financial year.

Consultancies with a contract value below $10,000 each

| Consultancies | Purpose | $ Actual payment |

|---|---|---|

| All consultancies below $10,000 each - combined | Various | 4,930 |

Consultancies with a contract value above $10,000 each

| Consultancies | Purpose | $ Actual payment |

|---|---|---|

| Scyne Advisory Pty Ltd | Internal Audit Services | 22,344 |

| Taylor Fry Pty Ltd | Scheme Actuary Services | 563,323 |

| Total | 585,667 |

See also the Consolidated Financial Report of the Department of Treasury and Finance (external site) (PDF) (external site) (PDF) for total value of consultancy contracts across the South Australian Public Sector.

The following is a summary of external contractors that have been engaged by the CTP

Regulator, the nature of work undertaken and the actual payments expensed for work

undertaken during the financial year.

Contractors with a contract value below $10,000

| Contractors | Purpose | $ Actual payment |

|---|---|---|

| All contractors below $10,000 each - combined | Various | 9,600 |

Contractors with a contract value above $10,000 each

| Contractors | Purpose | $ Actual payment |

|---|---|---|

| BizHub Australia Pty Ltd | CTP Claims Register Support | 43,952 |

| Chamonix IT Management Pty Ltd | Project Management Tool Development Support | 35,591 |

| Dr. Beata M Byok | MAIAS Reviewer Services | 13,297 |

| Haymakr | Claimant Service Rating Services | 56,818 |

| Healthcare Australia Pty Ltd | MAIAS Reviewer Services | 10,411 |

| Total | 160,069 |

The details of South Australian Government-awarded contracts for goods, services and works are displayed on the SA Tenders and Contracts website. View the agency list of contracts. (external site) (external site)

The website also provides details of across government contracts (external site) (external site).

Risk Management

The CTP Regulator’s Risk and Audit Committee meets quarterly to provide assurance to the

Governance Committee on the operation and effectiveness of the risk management

framework and internal and external audit activities.

The Regulator also reports annually to the Department of Treasury and Finance (DTF) Risk and Performance Committee.

In the past year, the Regulator’s Risk and Audit Committee fulfilled its responsibilities

according to its terms of reference, including:

- overseeing the 2023-24 internal audit plan (external independent auditor)

- acting on independent review of strategic risks by external auditor

- reviewing and updating the risk appetite statement

- maintaining the Risk Management Framework, risk management systems and processes

- reviewing and updating the Regulator’s Business Continuity Plan

- reviewing the Regulator's adherence to its legislated and contractual obligations

- overseeing the implementation of the Cyber Security Plan.

There was no fraud detected inside the Regulator.

The Regulator has a robust suite of policies and work instructions to address key risks and

establish controls to mitigate the risk of fraud. These controls include but are not limited to:

- segregation of duties

- delegations of authority

- user restrictions to financial software

- active management of information assets

- asset register

- triennial employee criminal history screening

- independent internal audit function

- financial management compliance program

- staff training and education on policies and procedures

- requirement of staff to adhere to the Public Sector Code of Ethics

- annual and ongoing conflict of interest declaration process for all staff.

Public interest disclosure for the CTP Regulator is reported directly to the DTF and is recorded and reported in the DTF annual report.

Note: Disclosure of public interest information was previously reported under the Whistleblowers Protection Act 1993 and repealed by the Public Interest Disclosure Act 2018 on 1/7/2019.

Reporting required under the Compulsory Third Party Insurance Regulation Act 2016

This section of the report details the operational activities performed to meet the Regulator’s functions under the Act.

Key activities completed in 2023-24 include:

- Updated the Scheme Rules, available on the CTP website. The Scheme Rules set out obligations for CTP Insurers and provide guidance for claimants and other scheme stakeholders about the operation of the Scheme.

The updated Scheme Rules were the result of extensive internal review and consultation with CTP Insurers. The focus of the review was to simplify for ease of reference for injured people, provide better regulation and reduce unnecessary regulatory burden. This was the first holistic review of the Scheme Rules since the beginning of the competitive scheme in 2019.

Consideration was also given to areas where regulation should be strengthened. Regulation has been strengthened particularly around insurer IT systems (through amendments to Commercial Rule 6) in light of increased focus on cyber security and the protection of information. - Reviewed and determined premium bands to apply from 1 January 2024 and from 1 July 2024. The review and determination for 1 January was the first time the Regulator undertook a mid-year review of CTP premiums which resulted in changes to premium bands. Most policy holders (99.9 percent of projected registered vehicles for 2024-25) were offered a lower CTP premium from 1 July 2024 compared to 1 July 2023.

- Took proactive steps to strengthen our cyber security governance and protection of scheme data. This included undertaking penetration testing of the CTP Claims Register, limiting the personal and sensitive information held by the Regulator to a minimum level of detail to meet business needs and improving our data storage and governance practices to minimise the exposure to potential cyber events.

- Conducted a thorough refurbishment of CTP website content. The website is the main method that the Regulator provides information to the general public, fulfilling our statutory function of providing information to consumers about the CTP insurance business. The aim of this work was to ensure that content on the Regulator’s website is as accessible and easy to understand as possible to improve the South Australian public’s understanding of the CTP Scheme. Website refurbishment included the

development of interactive tools to simplify the way information is provided to the public. - Published updated data to the Scheme Data Dashboard. The Dashboard provides an overview of the Scheme, including CTP claims and insurer premiums from 1 July 2016 up to 31 December 2023. The dashboard is updated annually.

- Published the annual 2024-25 SA CTP Market Briefing (PDF) (PDF) prepared by the independent scheme actuary, which informs the premium setting.

- Published the January to June 2024 SA CTP Market Briefing (PDF) (PDF). This was the first time the Regulator undertook a mid-year review of CTP premiums which resulted in changes to premium bands.

- Published the 2024-25 South Australia Point-to-Point Industry Relativities Briefing prepared by the independent scheme actuary, which outlines the relativities advice that informs the premium setting for vehicles in the point-to-point industry.

- Engaged with South Australian public hospitals (Royal Adelaide, Flinders Medical Centre, Lyell McEwin and the Women’s and Children’s) to provide information about the CTP Scheme to trauma nurses. This aimed to promote early intervention and improved health outcomes for eligible injured people through increased awareness of, and early access to treatment, care and support provided within the Scheme.

- Collaborated with the Lifetime Support Authority (LSA) to improve understanding of the CTP Scheme for LSA staff, so that they could better support injured people in the Lifetime Support Scheme who may also have a CTP claim and, when applicable, make the transition between the two schemes seamless for the injured person.

The Regulator uses a suite of tools to oversee and identify areas for further investigation in

scheme trends, CTP Insurer performance and data quality.

The Regulator monitors the compliance of CTP Insurers with contractual and legislative

obligations using the scheme compliance framework. The framework is risk-based, targeting areas of highest priority for the Scheme, and is primarily aimed at ensuring CTP Insurers actin the best interests of injured people and the CTP Scheme.

Areas of compliance focus are determined by the Regulator after reviewing and considering

the compliance performance of all CTP Insurers. This process is undertaken every two years.

Regulator compliance activities for 2023-24 included over 5,000 audit tests being applied. The main compliance activities prescribed by the framework in 2023-24 were:

- claims management reviews

- data analytics

- mandatory declarations

- CTP Insurer Business Plan reviews

- reviews in response to complaints

- injury coding reviews

The Regulator has continued its Insurer Compliance Program comprising a two-year cycle of full-scope insurer audits as well as targeted audits of specific claims management activities. Overall, the audits demonstrated high levels of insurer compliance with their legal and contractual obligations.

The scale and scope of the compliance program is proportionate with insurer performance

and supports keeping downward pressure on insurer regulatory costs.

The CTP Insurer audits address performance across the insurer’s business operation, including:

- service levels provided to claimants

- compliance with legislative obligations

- approval of treatment, care and support

- complaints management and dispute resolution

- payments and settlement

- privacy breaches and management of confidential information

- records management.

Areas of good performance include assisting injured people to lodge a claim, providing

claimants with information about their claim, notifying claimants when their Statement Giving Authority to Obtain Information (prescribed authority) will be used and providing claimants the information obtained using the prescribed authority, and communicating liability decisions to claimants in a timely manner.

Identified areas for improvement for insurers that were audited in 2023-24 include:

- records management

- proactively obtaining information for a CTP claim

- sending claim information to health professionals in a timely manner

- providing a written response to funding requests and clear reasons for denied funding requests.

Where the compliance program identifies unsatisfactory performance, a finding of noncompliance is made against the relevant scheme obligation. The outcome of a finding may result in no further action, a request for remediation, a Notice of Breach and/or a financial sanction. Where a CTP Insurer is required to submit a remediation plan, insurer performance against the remediation plan is tracked against agreed timeframes and outcomes monthly.

Six formal breaches were issued for the 2023-24 financial year. In response to CTP Insurer

breaches, two financial sanctions of $10,000 each were paid to the State Government.

| CTP Insurer | Breaches 2022-23 | Breaches 2023-24 |

|---|---|---|

| AAMI | 1 | 0 |

| Allianz | 1 | 0 |

| NRMA | 0 | 6 |

| QBE | 0 | 0 |

| Youi | 0 | 0 |

| Total | 2 | 6 |

Note – While CTP Insurers are required to report any self-identified breaches, the Regulator conducts audits of each insurer every two years and on an ‘as needed’ basis. This may lead to CTP Insurers subject to an audit in any given year having more breaches detected.

Continued oversight of insurers’ claims management practices has seen improvements in

insurers’ claimant service ratings (out of 100), increasing from 78 in last financial year to 81 in 2023-24, indicating improved insurer performance and scheme experience for injured people.

Enhancing the Regulator’s system for recording and monitoring insurer compliance was

identified as an action of strategic importance for the Scheme. The Regulator’s office worked with a vendor to develop an IT solution to support compliance activities and replace the previous auditing methods. The purpose-built system better supports the Scheme Compliance team’s audit processes and the overall robustness of scheme compliance monitoring.

The new system:

- Contains insurer audits in a single system.

- Improves efficiency of the audit process by enabling CTP Insurers to review their audit results and provide more information or further evidence directly into the system.

- Enables the Regulator to develop, store and maintain key elements of the Regulator’s Compliance Framework (obligations, audit tests, results, findings and regulatory actions) in a single database.

- Enables the Regulator to record, store and retrieve all historical compliance activity records from the database for any given obligation.

- Eliminates the need to manually review multiple documents across audit years to determine prior actions.

- Allows the Scheme Compliance team to easily link compliance activity results to audit recommendations and decisions, including the evidence that was relied upon to make those recommendations and decisions.

The new compliance management system will continue to support the Regulator’s oversight of CTP Insurers in future compliance activities.

Scheme efficiency review

Each year, the Regulator initiates an independent review of scheme efficiency to be conducted by the scheme actuary. The results are published in the CTP Scheme Efficiency Report as at 31 December 2023 (PDF) (PDF), available on the CTP Regulator’s website (www.ctp.sa.gov.au).

The review examines the efficiency of the CTP Scheme by evaluating the proportion of

customer premiums returned to injured people with CTP claims; this proportion is called the scheme efficiency index. The estimated scheme efficiency index increased from an average of 37% in the pre-competition period (1 July 2016 to 30 June 2019) to 52% since the introduction of competition (since 1 July 2019).

The review shows that the current competitive scheme is operating more efficiently than the previous scheme; providing supports to injured people at a lower cost to the South Australian community.

Review of the use of independent medical assessments in the Scheme

The Regulator undertook a review of a sample of independent medical assessments to

understand when, why and how they are being used in the Scheme. The objective of this

review was to gain better insight into the use of these independent assessments and the

potential impact on injured people, to identify opportunities to improve their experience.

Attending assessments can impact injured peoples’ experience within the Scheme, especially where the person does not understand the purpose of the assessment, when they have to attend multiple assessments, and when the assessment is used to resolve a dispute. independent assessments also contribute to scheme costs; therefore, the appropriate use of these assessments is important for both scheme experience and scheme efficiency.

The Regulator requested information from insurers on a sample of claims to understand:

- how, why and when independent medical assessments were used

- the prevalence and reason for multiple assessments

- the extent of insurer awareness about how and why assessments arranged by the injured person, or their representative, are used, and whether the injured person’s experience differs by who arranged the assessment

- whether there are any opportunities for the Regulator and/or insurers to support a

positive experience for injured people.

The review found that the industry is using assessments appropriately and when required.

The Guideline for Arranging Joint Independent Medical Assessments aims to assist with reducing the number of assessments the injured person may be asked to attend and supporting claimants through the process. The Regulator Rules require insurers to support and enhance the injured person’s experience when arranging independent assessments. These include considering the injured person’s individual circumstances; ensuring the choice of the assessor is based on medical reasoning; and providing information about the assessment to the injured person, including the reasons for attending.

The Regulator will continue to monitor insurers’ compliance with the Regulator Rules to

support a positive experience with independent assessments for injured people.

Insurer benchmarking review

The Regulator monitors scheme performance in a number of ways including, investigating

complaints, auditing insurers, conducting research and reviews, and insurer performance

benchmarking (assessing insurer performance against set standards and against each other).

In some areas of insurer benchmarking, the Regulator has assessed the private insurers’

performance against the performance of the Motor Accident Commission (MAC), which

managed claims under the previous scheme (prior to 1 July 2016). With the Scheme maturing and gaining sufficient past experience, benchmarks which are based on the performance of the MAC are being relied upon to a lesser degree.

A review was conducted on the existing liability timing benchmark, which was based on MAC data. This standard has been effective at driving insurer behaviour in making timely liability decisions. However, insurers typically outperform the service standard, making liability determinations sooner.

Ultimately the review resulted in an update to the liability timing minimum service standard

with a new industry standard based on private insurer performance over the last several years. This represents an important milestone for the Scheme to place more emphasis on current insurer performance and depart from reference back to the previous scheme. Moving to create new benchmarking standards based on the current scheme’s performance will impose higher standards for the CTP Insurers to meet.

The Regulator also created new benchmarking measures around claimants returning to work. There is regular monitoring of the percentage of claimants who need help returning to work, and the percentage of those that did return to work before their claim closed. These measures give the Regulator visibility of a key outcome of the Scheme and encourage better service from the insurers in this area.

In the CTP Scheme, an injured road user may be entitled to compensation for their injuries.

Some types of compensation, including non-economic loss and compensation for gratuitous services, are subject to thresholds based on the Injury Scale Value (ISV) of the injuries.

The South Australian Motor Accident Injury Accreditation Scheme (MAIAS) accredits medical

practitioners to undertake ISV medical assessments (Assessments) that assist in determining an injured person's entitlement to compensation.

The objective of the MAIAS is to create an independent system that provides consistent,

objective and reliable Assessments. The MAIAS accredits medical practitioners to undertake

Assessments which includes assigning ISV Item Numbers for each injury sustained in the

motor vehicle accident. The reports from these Assessments assist injured people and CTP

Insurers in the claims settlement process.

To be accredited by the MAIAS, medical practitioners must first be accredited under the

ReturnToWorkSA (RTWSA) scheme as an Impairment Assessor. The MAIAS collaborates with RTWSA to develop an integrated process for applications, training and developing assessor capability where appropriate, and has an interest in RTWSA’s Impairment Assessor Accreditation scheme more broadly.

Over the coming year, the MAIAS will continue to monitor RTWSA’s review of its Impairment

Assessment Guidelines and Impairment Assessor Accreditation Scheme to identify changes

that could impact the MAIAS. The MAIAS will also work with RTWSA to identify medical

specialties in need of more Accredited Medical Practitioners (AMPs) to assess injuries and

provide injured people with greater access to the appropriate specialty.

In early 2024, the CTP Regulator recruited an Injury Services Officer to support the work of the MAIAS Administrator. The Injury Services Officer is responsible for coordinating the work of the MAIAS, including overseeing accreditations and managing the quality assurance (QA) program.

In 2023-24, the MAIAS Administrator conducted QA reviews to assess the quality of ISV medical assessment reports (Reports) against the requirements of the Civil Liability Act 1936, Civil Liability Regulations 2013, MAIAS Rules and the criteria in the MAIAS Training Manual 3rd Edition.

During the QA program, 85 physical Reports and 16 pure mental harm Reports were reviewed by medical expert peer reviewers. The review found areas for improvement, including stating stability for each referred injury, addressing all referred injuries, accurately calculating and explaining the basis for the assigned Whole Person Impairment or Guide to the Evaluation of Psychiatric Impairment for Clinicians (GEPIC) rating, and providing clear rationale for selecting the assigned ISV Item Numbers.

Assessed AMPs can seek further feedback on their QA findings and engage with the peer

reviewers, if required. They may also revisit training materials through the MAIAS learning

management system at any time.

Over the 2024-25 financial year, the MAIAS will review the current QA program to identify

opportunities for improvement.

The QA program is conducted with assistance from medical experts who are experienced in their field (peer reviewers). In September 2023, the MAIAS engaged a new peer reviewer to support the QA program.

Insured vehicles by type

Registrations as at 30 June 2024

| Type of vehicle | Vehicles | % |

|---|---|---|

| Private passenger | 1,141,388 | 56.66% |

| Public passenger: no fare | 636 | 0.03% |

| Taxis: metropolitan | 1,052 | 0.05% |

| Taxis: country | 245 | 0.01% |

| Hire cars | 11,341 | 0.56% |

| Rideshare: country | 2 | 0.00% |

| Rideshare: metropolitan | 4,867 | 0.24% |

| Public passenger: small | 714 | 0.04% |

| Public passenger: medium | 1,087 | 0.05% |

| Public passenger: heavy | 694 | 0.03% |

| Public passenger: omnibus | 1,024 | 0.05% |

| Goods carrying: light | 251,025 | 12.46% |

| Goods carrying: medium | 16,636 | 0.83% |

| Goods carrying: heavy | 11,539 | 0.57% |

| Goods carrying: primary producers | 30,952 | 1.54% |

| Motorcycles: ultra light | 3,040 | 0.15% |

| Motorcycles: light | 8,325 | 0.41% |

| Motorcycles: medium | 14,018 | 0.70% |

| Motorcycles: heavy | 20,838 | 1.03% |

| Tractors | 54,067 | 2.68% |

| Historic and left hand drive vehicles | 46,968 | 2.33% |

| Special purpose vehicles | 17,484 | 0.87% |

| Car carriers: light | 3 | 0.00% |

| Car carriers: medium | 18 | 0.00% |

| Car carriers: heavy | 1 | 0.00% |

| Car carrier trailers | 122 | 0.01% |

| Trailers | 374,211 | 18.58% |

| Unregistered vehicle permits | 117 | 0.01% |

| Motor trade plate | 2,119 | 0.11% |

| Total | 2,014,533 | 100.00% |

Source: Department for Infrastructure and Transport policy data.

Ratio of class 1 premium(1) to South Australian average weekly earnings (AWE)(2)

| Annual premium(1) | State AWE(2) | Ratio | |

|---|---|---|---|

| 2023-24 | $270.78 | $1,735 | 16% |

| 2022-23 | $294.99 | $1,658 | 18% |

| 2021-22 | $290.33 | $1,591 | 18% |

| 2020-21 | $295.40 | $1,543 | 19% |

| 2019-20 | $296.77 | $1,504 | 20% |

| 2018-19 | $411.25 | $1,462 | 28% |

(1) Note: Premium is the weighted average lowest priced Class 1 District 1 public passenger vehicle (private use, no input tax entitlement) on offer over the financial year.

(2) Source: Australian Bureau of Statistics, 6302.0 Average Weekly Earnings, Australia. Earnings; Persons; Full Time; Adult; Ordinary time earnings; South Australia; Series Id: A84989336X, November (in given financial year).

Premium and fee collection

1 July 2023 to 30 June 2024

| Description | $'000 |

|---|---|

| Insurers' premiums* | 310,119 |

| Stamp duty | 42,341 |

| Road safety | 14,051 |

| Emergency transport, hospital and forensic services | 38,105 |

| Customer support and transaction processing | 11,292 |

| CTP Scheme regulation and administration | 6,495 |

| Total insurance premiums collected | 422,402 |

Note: *Includes GST.

Market share of in-force premium

| AAMI | Allianz | NRMA | QBE | Youi† | |

|---|---|---|---|---|---|

| 30 June 2024 | 29% | 21% | 19% | 26% | 5% |

| 30 June 2023 | 32% | 7% | 25% | 29% | 7% |

| 30 June 2022 | 40% | 9% | 30% | 21% | |

| 30 June 2021 | 20% | 18% | 41% | 21% | |

| 30 June 2020 | 28% | 27% | 24% | 21% | |

| 30 June 2019* | 30% | 15% | 20% | 35% |

Note: *All insurers had contractually agreed market share for the first three years of the privately underwritten scheme – 2016 to 2019.

†Youi entered the Scheme on 1 July 2022.

Number of changes to filed premiums 2023-24

| Type of vehicle | District 1 | District 2 |

|---|---|---|

| Private passenger | 12 | 11 |

| Public passenger: no fare | 4 | 6 |

| Taxis: metropolitan | 4 | |

| Taxis: country | 6 | |

| Hire cars | 9 | 9 |

| Rideshare: country | 3 | |

| Rideshare: metropolitan | 4 | |

| Public passenger: small | 4 | 6 |

| Public passenger: medium | 4 | 6 |

| Public passenger: heavy | 4 | 6 |

| Public passenger: omnibus | 6 | |

| Goods carrying: light | 12 | 11 |

| Goods carrying: medium | 10 | 13 |

| Goods carrying: heavy | 12 | 11 |

| Goods carrying: primary producers | 10 | 4 |

| Motorcycles: ultra light | 7 | 7 |

| Motorcycles: light | 8 | 8 |

| Motorcycles: medium | 7 | 7 |

| Motorcycles: heavy | 5 | 9 |

| Tractors | 6 | 6 |

| Historic and left hand drive vehicles | 4 | 6 |

| Special purpose vehicles | 5 | 7 |

| Car carriers: light | 4 | 2 |

| Car carriers: medium | 4 | 2 |

| Car carriers: heavy | 4 | 2 |

| Car carrier trailers | 6 | 2 |

| Unregistered vehicle permits | 2 | 2 |

| Total | 166 | 143 |

This is an indicator of premium price competition in the CTP Scheme. Premium classes for taxis, rideshare and omnibuses do not depend on the district, but are counted with district 1 in the table.

Note: 2023-24 had more changes to filed premiums than previous years in part because the premium bands were reviewed and updated from 1 January, requiring all insurers to re-file for every vehicle class.

Claimant service rating results

| Publication month | AAMI | Allianz | NRMA | QBE | Youi† |

|---|---|---|---|---|---|

| June 2024 | 82 | 81 | 80 | 83 | 79 |

| June 2023 | 84 | 75 | 77 | 77 | |

| June 2022 | 84 | 78 | 74 | 80 | |

| June 2021 | 77 | 78 | 79 | 75 | |

| June 2020 | 81 | 72 | 85 | 77 | |

| June 2019 | 69 | 72 | 70 | 71 |

Note: The score published each month is the average claimant service rating from claimants surveyed in the previous six to twelve months.

†Youi entered the Scheme on 1 July 2022 and its claimant service rating was only published once enough claimants had been surveyed to give a representative sample.

Number of accidents by region

1 July 2023 to 30 June 2024

| Region | Accidents | % |

|---|---|---|

| Adelaide City / Suburbs | 1,439 | 86.5% |

| Outer Adelaide | 113 | 6.8% |

| Murraylands | 30 | 1.8% |

| South | 16 | 1.0% |

| Northern | 10 | 0.6% |

| Eyre | ||

| Interstate | ||

| Total |

Note: The recent accident years’ data is immature due to accidents where a claim is yet to be reported.

Claim lodgement by development year

1 July 2016 to 30 June 2024

| Development Year | |||||||

|---|---|---|---|---|---|---|---|

| Accident Year | 1 | 2 | 3 | 4 | 5 | 6+ | Total |

| 2016-17 | 2376 | 631 | 49 | 29 | 16 | 7 | 3108 |

| 2017-18 | 2115 | 470 | 56 | 21 | 5 | 9 | 2676 |

| 2018-19 | 1934 | 427 | 45 | 19 | 15 | 7 | 2447 |

| 2019-20 | 1557 | 343 | 52 | 31 | 18 | 2001 | |

| 2020-21 | 1,730 | 436 | 29 | 31 | 2226 | ||

| 2021-22 | 1532 | 368 | 50 | 1950 | |||

| 2022-23 | 1592 | 357 | 1949 | ||||

| 2023-24 | 1870 | 1870 | |||||

| Total | 18,277 | ||||||

Note: Development year 1 means claims lodged in the accident year (year means financial year), development year 2 means claims lodged in the year after the accident year, etc.

Claims by current status

1 July 2016 to 30 June 2024

| Accident year | Claims lodged | Claims open | Claims closed | % closed |

|---|---|---|---|---|

| 2023-24 | 1,870 | 1373 | 497 | 27% |

| 2022-23 | 1949 | 854 | 1,095 | 56% |

| 2021-22 | 1,950 | 591 | 1,359 | 70% |

| 2020-21 | 2,226 | 384 | 1,842 | 83% |

| 2019-20 | 2,001 | 233 | 1,768 | 88% |

| 2018-19 | 2,447 | 123 | 2,324 | 95% |

| 2017-18 | 2,676 | 69 | 2,607 | 97% |

| 2016-17 | 3,108 | 35 | 3,073 | 99% |

Claimants by demographic

1 July 2016 to 30 June 2024

| Age group | Males | Females | Total | % |

|---|---|---|---|---|

| 16 years and under | 406 | 424 | 832 | 5% |

| 17 to 24 years | 934 | 1,296 | 2,239 | 12% |

| 25 to 34 years | 1,558 | 1,989 | 3,550 | 19% |

| 35 to 44 years | 1,484 | 1,791 | 3,283 | 18% |

| 45 to 54 years | 1,587 | 1,792 | 3,387 | 19% |

| 55 to 64 years | 1,317 | 1,346 | 2,670 | 15% |

| 65 years and over | 955 | 1,301 | 2,261 | 12% |

| Unspecified | 3 | 2 | 5 | 0% |

| Total | 8,244 | 9,941 | 18,227 | 100% |

Claimants by accident role

1 July 2016 to 30 June 2024

| Role | Claims | % |

|---|---|---|

| Driver | 11,579 | 64% |

| Passenger | 3,895 | 21% |

| Bicyclist | 1,263 | 7% |

| Pedestrian | 1,195 | 7% |

| Other | 295 | 2% |

| Total | 18,227 | 100% |

Claims by severity

Closed claims for accidents from 1 July 2016 to 30 June 2024

| AIS* severity | Claims | % |

|---|---|---|

| Minor | 9,394 | 64.5% |

| Moderate | 1,897 | 13.0% |

| Serious | 727 | 5.0% |

| Severe | 60 | 0.4% |

| Critical | 27 | 0.2% |

| Maximum | 226 | 1.6% |

| Admin Only | 2,234 | 15.3% |

| Total | 14,565 | 100.0% |

Note:

*Injury severity based on injuries coded under the Abbreviated Injury Scale (AIS) 2005 and the Update 2008 Manual.

“Minor” category includes claims where a regionspecific injury code was reported with a severity of 9 (“not further specified”).

“Maximum” injury severity usually indicates a fatality.

“Admin” means there were no physical injuries caused by the accident or there was no medical evidence available for injury coding.

Claims by dominant injury body region

Closed claims for accidents from 1 July 2016 to 30 June 2024 excluding claims without a dominant injury recorded

| Body region | Claims | % |

|---|---|---|

| Cervical spine | 3,434 | 25% |

| Shoulder | 2,905 | 21% |

| Thoracic spine or lumbar spine | 1,734 | 13% |

| Other | 1,352 | 10% |

| Pelvis or hip | 1,049 | 8% |

| Other lower limb | 725 | 5% |

| Pure mental harm | 684 | 5% |

| Knee | 629 | 5% |

| Central nervous system and head | 512 | 4% |

| Chest | 370 | 3% |

| Wrist | 363 | 3% |

| Total | 13,757 | 100% |

Rates of legal representation

1 July 2016 to 30 June 2024

| Accident year | Claims | % Legal rep | % Litigated | % Trial |

|---|---|---|---|---|

| 2023-24 | 1,870 | 23% | 0% | 0.00% |

| 2022-23 | 1,949 | 30% | 0% | 0.00% |

| 2021-22 | 1,950 | 35% | 1% | 0.00% |

| 2020-21 | 2,226 | 39% | 14% | 0.00% |

| 2019-20 | 2,001 | 40% | 17% | 0.00% |

| 2018-19 | 2,447 | 35% | 15% | 0.00% |

| 2017-18 | 2,676 | 41% | 17% | 0.04% |

| 2016-17 | 3,108 | 41% | 20% | 0.03% |

Note: The recent accident years’ data is immature due to the long tail nature of CTP claims

Legal costs

All legal cost payments for accidents from 1 July 2016 to 30 June 2024

| Accident year | Solicitor client costs | Plaintiff - Legal ($'000) | Defendant - Legal ($'000) | Grand total ($'000) |

|---|---|---|---|---|

| 2023-24 | Unknown | - | 45 | 45 |

| 2022-23 | Unknown | 348 | 274 | 622 |

| 2021-22 | Unknown | 2,204 | 722 | 2,926 |

| 2020-21 | Unknown | 6,826 | 3,027 | 9,853 |

| 2019-20 | Unknown | 9,213 | 4,767 | 13,980 |

| 2018-19 | Unknown | 12,038 | 6,585 | 18,623 |

| 2017-18 | Unknown | 18,344 | 9,563 | 27,907 |

| 2016-17 | Unknown | 20568 | 12355 | 32923 |

| Total | Unknown | 69,541 | 37,338 | 106,879 |

Note: Solicitor client costs are reported as unknown because there is no legal requirement for a solicitor to provide their solicitor client costs to the managing insurer of a claim or the CTP Regulator.

Claim duration by CTP Insurer

Closed claims for accidents from 1 July 2016 to 30 June 2024 where relevant data is available

| Timeframe (average days) | AAMI | Allianz | NRMA | QBE | Average |

|---|---|---|---|---|---|

| Notification date to compliance date | 44 | 74 | 51 | 15 | 41 |

| Notification date to liability decision date | 115 | 96 | 108 | 114 | 109 |

| Notification date to closure date | 534 | 589 | 483 | 581 | 542 |

Note: Youi’s claim portfolio is currently too underdeveloped to compare with the rest of industry.

Breakdown by heads of damage

Closed claims from 1 July 2023 to 30 June 2024 for accidents from 1 July 2016 to 30 June 2024

| Heads of damage | Closed claims | Total ($’000) | % Closed payments |

|---|---|---|---|

| Economic Loss | 997 | $84,575 | 48.6% |

| Non-Customer Benefits | 1,768 | $35,148 | 20.2% |

| Treatment | 2,043 | $25,998 | 14.9% |

| Care | 973 | $19,297 | 11.1% |

| Non-Economic Loss | 421 | $7,633 | 4.4% |

| Other Customer Benefits | 679 | $1,313 | 0.8% |

| Total | 2,181 | $173,964 | 100.0% |

Note:

“Care” category includes payments for past and future care and home services, care-related travel and voluntary services.

“Non-customer benefits” category includes investigation costs, the costs of medical reports from treating medical providers and ISV medical assessors, and plaintiff and defendant legal costs.

“Other customer benefits” category includes claimant travel expenses and reasonable funeral costs.

“Treatment” category includes payments for past and future medical, allied health and hospital services, excluding public hospital services funded from the administrative fee component of CTP premiums.

Nil claims (zero payments) have been excluded from the data.

Nominal defendant claims received by accident year

Accidents from 1 July 2016 to 30 June 2024

| Year of accident | Unidentified vehicles | Unregistered vehicles | Total |

|---|---|---|---|

| 2023-24 | 70 | 10 | 80 |

| 2022-23 | 57 | 12 | 69 |

| 2021-22 | 60 | 12 | 72 |

| 2020-21 | 70 | 12 | 82 |

| 2019-20 | 61 | 11 | 72 |

| 2018-19 | 71 | 10 | 81 |

| 2017-18 | 78 | 14 | 92 |

| 2016-17 | 95 | 12 | 107 |

Note: The recent accident years’ data is immature due to accidents where a claim is yet to be reported. Data for previous years has changed slightly since last year’s annual report due to data cleanup.

Communications

| Type | Number of instances |

|---|---|

| Complaints about CTP Insurers | 26 |

| Complaints about the Scheme | 1 |

| Complaints about the Motor Accident Injury Accreditation Scheme (MAIAS) | 0 |

| Complaints about the Regulator | 1 |

| Total | 28 |

| Enquirer source | Number of enquiries |

|---|---|

| General public | 1,845 |

| CTP Insurer | 477 |

| Medical | 470 |

| Legal | 142 |

| Government Department | 104 |

| Other | 7 |

| Total | 3,045 |

| Type | Average time taken to be resolved (in business days) |

|---|---|

| Enquiries & feedback | 0.4 |

| Complaints | 3.8 |

| Enquiry category | Number of enquiries |

|---|---|

| Claims | 1,052 |

| CTP Scheme | 269 |

| Non-CTP-related enquiries* | 209 |

| Operations | 113 |

| Suspected fraud, scamming or deception | 73 |

| Nominal Defendant | 70 |

| Complaints | 56 |

| MAIAS | 3 |

| Total | 1,845 |

Note: *Enquiries about topics outside of the Regulator’s scope, for example, comprehensive vehicle insurance, vehicle registration, or road safety.

The number for ‘complaints’ does not match the number of complaints listed in the public complaints section of this annual report because each complaint can involve multiple interactions. This category also includes questions about the complaints process that do not result in a formal complaint being lodged with the Regulator.